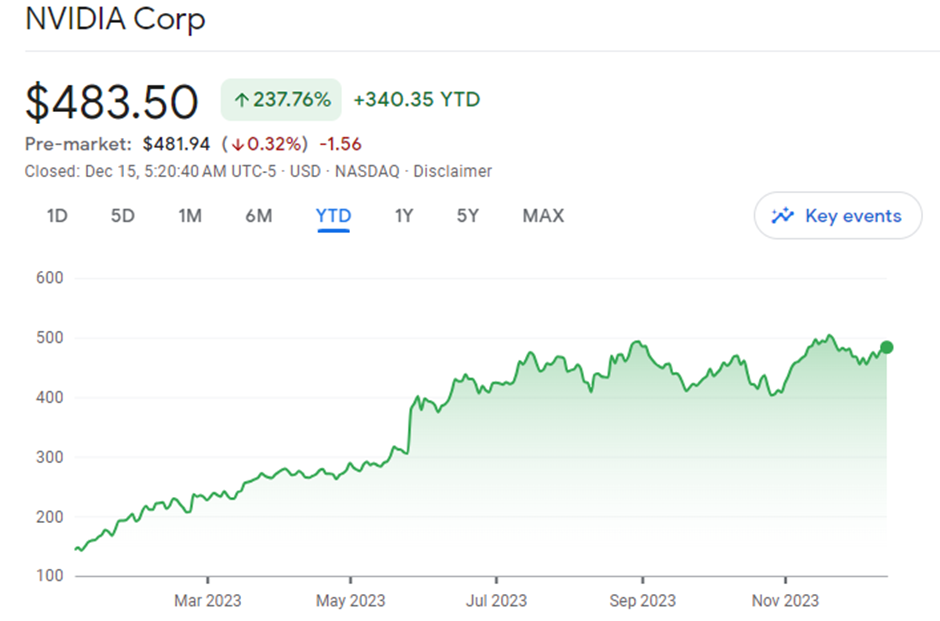

With a share price return this year of nearly 240%, NVIDIA has been the stock that everyone has talked about.

This has been a classic momentum play that doesn’t pay much attention to the trailing valuation multiples (i.e. based on historical rather than future numbers), although a look at the share price chart does show that the stock has been consolidating in a range of $400 to $500 since June:

Source: Google Finance

For those who enjoy dabbling in range trading opportunities, buying that support level at around $400 has been a lovely strategy. Buying at close to $500 has clearly not worked out so well, which is why you should always be looking at charts whether you are a short-term or long-term investor. They help with tactical decisions around entry and exit points.

Special calls for a special story

When a company is red hot in the market, you’ll see a great deal of effort going into telling the story. NVIDIA’s last earnings call was on 21 November. Since then, the company has presented at three technology conferences and hosted a further three special calls. Investors just cannot get enough of this.

And of course: there’s one buzzword driving all of this interest in NVIDIA: Artificial Intelligence. On one of the calls, an NVIDIA executive referred to the “official ChatGPT moment” that the world witnessed right at the end of 2022. Yes, it’s been a year already.

A lot can happen in a year. A lot has certainly happened to the NVIDIA share price, although it’s definitely worth highlighting that the five-year compound annual growth rate (CAGR) leading up to January 2023 was 19.9% and that’s after the ugly post-pandemic correction. It’s not like NVIDIA was an obscure business that suddenly emerged from the shadows

What’s that saying about an overnight success, ten years in the making?

Speaking of the share price, the pandemic peak of roughly $300 a share feels like a blip on the radar with the stock now trading at over $480. Of course, the real question is whether NVIDIA can make a sustainable break above $500. Linked to that, we have to consider the risk of a move below $400 at the bottom of the current traded range.

A whole new world

Apologies for an Aladdin reference that might be triggering for anyone who holds Disney shares. I have them too, so I feel your pain.

NVIDIA sits right at the centre of the AI revolution. The effect of this is a vastly expanded TAM, or Total Addressable Market. NVIDIA’s technology has landed beautifully in a client base that has literally exploded in size.

In a recent blog on the NVIDIA website, the company quotes research from Stanford that highlights that GPU performance has increased roughly 7,000 times since 2003. Now, that’s admittedly 20 years’ worth of improvement in an age of hyper-progress in technology, but it’s still a useful reminder that this stuff doesn’t follow a linear growth pattern.

I am certainly not going to make any claims to be an expert in this space, or even a novice. What I do understand is that generative AI is now on the lips of practically every large company in the world, so NVIDIA is perfectly positioned as the shovel in the gold rush. Being far up the value chain in an age of new technology is a concept that I do understand.

AI is the new and exciting toy for everyone to play with and NVIDIA is happily running a toy store, working directly with companies like Microsoft (and thus OpenAI) to deliver this new world of computing. If smartphones were the story of the past 10 – 15 years, then AI looks set to dominate the next decade.

But does this make NVIDIA a guaranteed winner? Can anything go wrong?

This isn’t a competitive vacuum, but there’s been a clear winner

The trouble with a “perfect story” like NVIDIA is that investors want to believe that the good times can carry on forever. It’s rare for a company to enjoy an unassailable competitive advantage for even a few years, let alone a decade. Even a company like Apple has numerous competitors. If you dig into Apple’s share price performance over the past decade, you’ll find that most of it has come from an increase in the valuation multiple rather than spectacular earnings growth.

We are seeing much the same story play out at Tesla. First mover advantage can be very helpful but doesn’t last forever. If there are juicy profits to be made, then you can be sure that competitors won’t be far away. Share prices may take a long time to reflect this reality, but those inefficiencies and human emotions create the opportunities in the market that we spend our time trying to find.

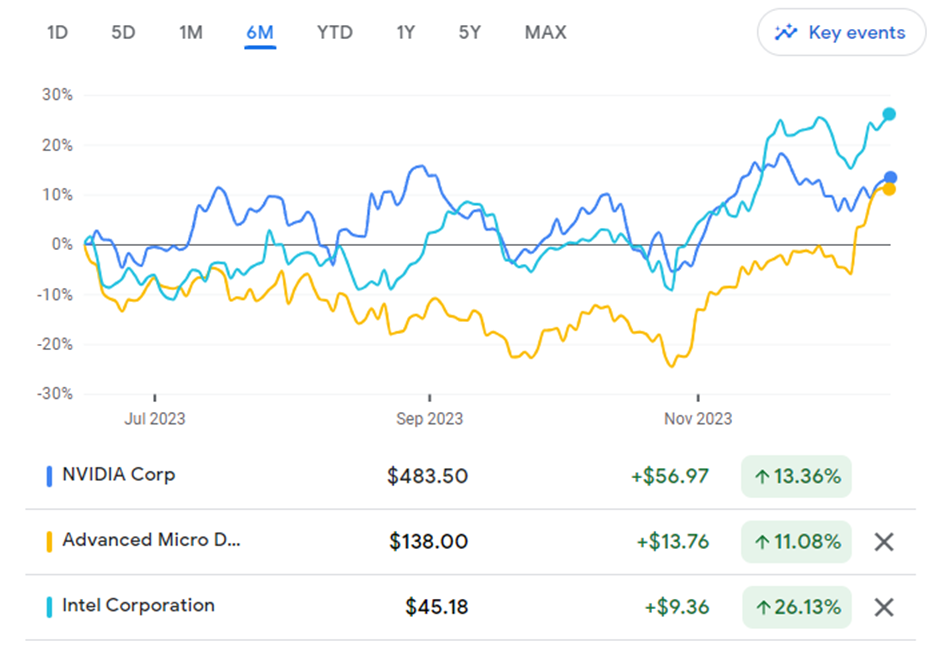

AMD is nowhere near the level of NVIDIA at the moment in terms of technological ability in AI, yet the correlation in the share prices can be eyeballed quite easily in the next chart. Remember, correlation doesn’t just mean that they have delivered the same performance; it’s about the shape of the charts and how they move together.

Relative performance is clearly in favour of NVIDIA, but they’ve both been somewhat range-bound since June:

Source: Google Finance

I simply can’t resist sharing a five-year chart that shows NVIDIA and AMD against Intel, which by all accounts should’ve been a worthwhile competitor. In the technology sector, when a company loses, it tends to lose in a big way:

Source: Google Finance

Intel has been left for dead. And yet, despite this, the range-bound nature of NVIDIA and AMD in the second half of 2023 created an opportunity for Intel to outperform over the smallest of time periods:

Source: Google Finance

This proves something that experienced market participants already know: timing the market is absolutely crucial when you have a short-term view. This is why traders spend a lot more time on charts than on fundamentals. As your time horizon increases, fundamentals and industry dynamics become far more important than the charts.

If you really want to unlock success in the markets, it helps tremendously to learn the differences between trading and investing and use both skillsets in assessing opportunities.

Let’s look at the numbers

In the November earnings call, NVIDIA reported revenue growth of 38%. That’s sequential growth, not annual growth. In other words, Q3 revenue was 38% higher than Q2, which is mildly insane. In case you’re wondering, annual growth was over 200%.

A hyper-scaling environment means hyper-scaling revenue. Gaming revenue of over 80% year-on-year seems pedestrian compared to what we are seeing in the AI side of NVIDIA’s business, yet that is also still a phenomenal growth rate. Gaming has doubled relative to pre-COVID levels despite low industry performance in PC sales. NVIDIA’s products are good enough that gamers buy them as separate components.

Revenue is great, but do they make any money? Well, GAAP gross margin (which is the right metric to look at) is a rather ridiculous 74%. In other words, for every $100 in sales (on average – as it will vary significantly by segment), NVIDIA generates $74 in gross profit to cover operating costs and reward investors.

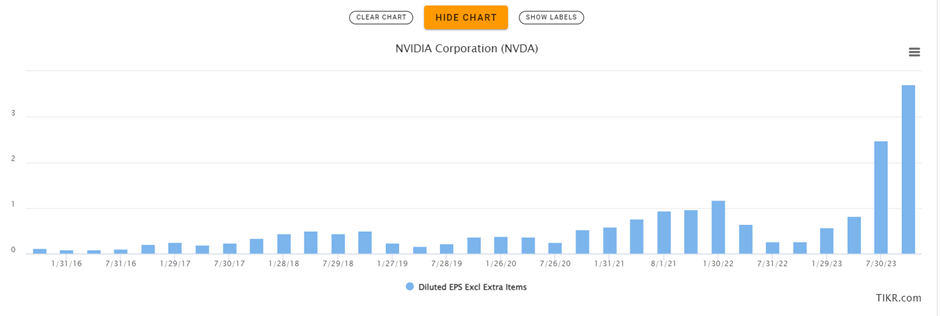

With growth like this at such high margins, it’s very important to see the gross profits actually dropping to the bottom line. There are far too many technology companies out there that are big on revenue growth and light on profits.

As this chart of quarterly earnings per share demonstrates, this isn’t the first time we’ve seen an uptick in diluted earnings per share at NVIDIA. But, it’s the first time that we’ve seen anything close to this magnitude:

Source: TIKR

So, to answer the question, NVIDIA does indeed make money. It makes a huge amount of money.

A flywheel that can keep spinning

On the earnings call, there was a great question from an analyst who beautifully summarised what success looks like for technology groups. I’ll quote Harlan Sur of JPMorgan directly:

“If you look at the history of the tech industry, right, those companies that have been successful have always been focused on ecosystem, silicon, hardware, software, strong partnerships and just as importantly, right, an aggressive cadence of new products, more segmentation over time. The team recently announced a more aggressive new product cadence and data center from 2 years to now every year with higher levels of segmentation, training, optimization, inferencing, CPU, GPU, DPU networking. How do we think about your R&D OpEx growth that looks to support a more aggressive and expanding forward road map? But more importantly, what is the team doing to manage and drive execution through all of this complexity?”

The first part of the question is exactly what NVIDIA is doing, with the added benefit of bringing down costs for clients as the business scales. Jensen Huang (the CEO of NVIDIA) loved the question and delivered a long answer, but the end is really the bit that counts:

“But the thing that really holds it together, and this is a great decision that we made decades ago, which is everything is architecturally compatible. When you -- when we develop a domain-specific language that runs on one GPU, it runs on every GPU. When we optimize TensorRT for the cloud, we optimized it for enterprise. When we do something that brings in a new feature, a new library, a new feature or a new developer, they instantly get the benefit of all of our reach.

And so that discipline, that architecture compatible discipline that has lasted more than a couple of decades now is one of the reasons why NVIDIA is still really, really efficient. I mean we're 28,000 people large and serving just about every single company, every single industry, every single market around the world.”

The number of staff really stuck with me. NVIDIA has just 28,000 people and has a market cap of $1.19 trillion. It’s an extraordinary story.

Is it extraordinary enough to pay a trailing EBITDA multiple of 54x for? How about a trailing free cash flow multiple of 85x? According to TIKR, consensus earnings suggest that those forward multiples are 27.5x and 27.8x respectively. Not only are these multiples expected to unwind very quickly (i.e. drop considerably as the company grows), but the relative convergence of free cash flow and EBITDA is fascinating.

Some stories are worth believing in

With a long-term lens, you would have to be a real luddite to think that AI isn’t going to play a huge role in the next decade of our lives. Although there are multiple ways to play the trend (including getting closer to the customers using the products, through companies like Microsoft and Salesforce), NVIDIA really is pulling off an incredible outcome for investors.

I never advocate for closing your eyes to the valuation of a stock. It’s a slippery slope indeed. In this case, the trailing multiples are pointless and only the forward multiples matter. Assuming NVIDIA can deliver on forecasts, it seems like there is a decent chance that the stock can break above $500 next year, particularly if the promised rate cuts from the Fed come to pass.

Yes, this outlook is more of a growth style than a value style, but in this case it seems warranted. It would just be lovely if NVIDIA would drop closer to $400 again to create another entry opportunity. It’s quite possible that anyone waiting for that level will be waiting forever!

The Finance Ghost has held and sold NVIDIA in the past 12 months. He does not currently have direct exposure to the stock but does have significant indirect exposure through certain ETFs.

Want to know more about the latest research?

Any opinions, news, research, reports, analyses, prices, or other information contained within this research is provided by an external contributor as general market commentary and does not constitute investment advice for the purposes of the Financial Advisory and Intermediary Services Act, 2002. First World Trader (Pty) Ltd t/a EasyEquities (“EasyEquities”) does not warrant the correctness, accuracy, timeliness, reliability or completeness of any information (i) contained within this research and (ii) received from third party data providers. You must rely solely upon your own judgment in all aspects of your investment and/or trading decisions and all investments and/or trades are made at your own risk. EasyEquities (including any of their employees) will not accept any liability for any direct or indirect loss or damage, including without limitation, any loss of profit, which may arise directly or indirectly from use of or reliance on the market commentary. The content contained within is subject to change at any time without notice.

Search all articles

Posts by topic

- Market News & Events

- Easy Community

- Education

- Dividends Update

- Exchange Traded Funds (ETFs)

- Property Investing

- Managed Bundles

- USD Wallet

- Retirement Annuity (RA)

- Cryptocurrency

- Tax Free Savings Account (TFSA)

- International Investing

- Unit Trusts

- New to Investing

- Artificial Intelligence

- EasyProtect

- EasyCredit

- Shares

- Government Bonds

- New Listings