With a special distribution coming in January, how do these value unlock opportunities work and why should investors be paying attention?

RMB Holdings. Take that image of the banking giant in Sandton out of your head immediately. The historical link isn’t reflective of the current state of play, with RMB Holdings (frequently called RMH – perhaps to try address the RMB confusion) now focused on property operations and returning value to shareholders.

That may sound odd to you. After all, shouldn’t all companies be focused on returning value to shareholders?

The difference here is that RMB Holdings isn’t talking about long-term growth strategies and those types of things. Instead, it’s all about managing the portfolio in such a way that shareholders get the best possible outcome before the listed entity is eventually wound up. This is commonly known as a “value unlock” strategy for obvious reasons.

Of course, the journey to achieve that value unlock is far from guaranteed. This is why the company trades at a discount to net asset value. There’s a big difference between a net asset value on paper and a cash payout to shareholders equal to that value.

Speaking of cash payouts…

How is value returned to shareholders?

A value unlock strategy often results in special distributions or dividends, with the company making payouts to shareholders as assets are disposed of. Investors look closely at the price achieved for the assets, particularly relative to the net asset value and what management told the market those assets are worth.

Where an investment holding company going through a value unlock process holds shares in other listed companies, you might see unbundling transactions as well. This is a game of passing the parcel, with the company distributing the investment in listed shares to its own shareholders. A good example of this was RMH unbundling its shares in FirstRand to its shareholders during the pandemic. I cannot stress enough that this is only appropriate where the shares being unbundled are also listed, otherwise shareholders would suddenly end up with an investment in a private company.

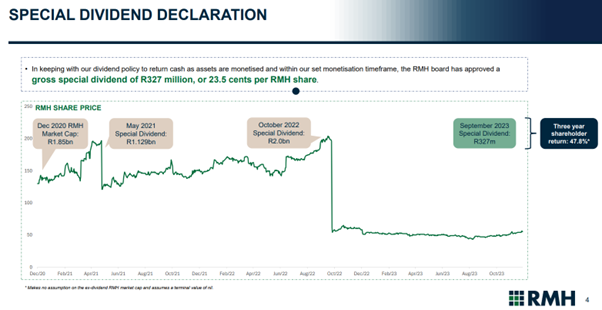

In both these cases, simply looking at the share price of RMH over time wouldn’t tell the right story. A special distribution causes a significant drop in the share price, as the company has effectively handed a large part of its value over to shareholders. Ditto for an unbundling, where value is shifted out of the company.

There’s a very helpful slide from the last investor presentation that shows how a share price is impacted by special dividends, with the same principle applicable to unbundlings:

To properly assess the return, you would need to add back the value of special dividends and unbundled shares. This would take you to an important concept called the total return, which is actually the right way to look at all investments, even though investors tend to ignore dividends when quoting share price performance.

Janu-worry: made easier by a special distribution

RMH has recently declared a gross special dividend of 23.5 cents per share. This will be subject to dividend withholding tax, so individual shareholders will receive 18.80 cents per share after tax. The share price at time of writing is 65 cents, so this shows how significant these distributions can be.

On the date on which the shares “go ex-div” – i.e. start trading without an entitlement to this distribution – you can expect the share price to drop by roughly the value of the gross dividend, as explained by the chart above. This will happen on Wednesday 24 January, so don’t get a big fright if you see your shares drop substantially on that day! The payment will be in your brokerage account on 29 January, just in time for those final pesky debit orders. Of course, the hope is that you’ve got your savings linked up for Janu-worry so that you can reinvest the distribution in something else!

Now, we need to take a closer look at what will still be left in RMB Holdings.

Property, property and more property

The remaining assets in RMH are in the property sector, held across three property vehicles. You might’ve seen a lot of noise around the investment in Atterbury Property Holdings this year, as RMH has been navigating a difficult situation with that company. When it comes to business, shareholders aren’t always aligned. In fact, they sometimes end up in scenarios where they are conflicted, creating tricky problems.

After much legal wrangling in 2023, Atterbury settled the balance of a loan from RMH by issuing additional shares at a price based on the net asset value of Atterbury. This increased RMH’s stake in Atterbury from 27.5% to 38.5%.

The investment in Atterbury represents the majority of the assets in RMH. Integer and Divercity are the other two property vehicles and are much smaller contributors to the story. Those investments combined were 17.5% of the group net asset value as at 30 September 2023, so they are material but not critical. It’s not hard to see why so much focus was placed on the Atterbury investment.

The Atterbury portfolio includes a 20% undivided share in Mall of Africa (a great property in my opinion), along with exposure to various other retail and office buildings in various cities. There’s even a retail property in Namibia!

Divercity holds a portfolio of mixed-use assets in Johannesburg. This is inner city stuff and the Joburg property market isn’t exactly a glowworm of happiness on a good day, so this might not be the easiest portfolio to monetise. In a recent capital raise by Divercity, RMH didn’t follow its rights and its stake diluted to 7.17% as a result.

Integer holds three assets. It’s a mixed bag of note, with an office building in Joburg, the Robertson and Caine yacht warehouse in Cape Town and a residential development in Joburg as well. Integer has been selling off assets one by one, as it’s very hard to find a buyer who would be interested in such an odd mix of properties.

As you can see, RMH doesn’t have a coherent property strategy. This mosaic of properties is therefore not easy to dispose of, particularly in a way that returns maximum value to shareholders. This can create tension over time, as investors put pressure on management to get on with it and sell the assets. There aren’t always buyers available, particularly at the right price.

This begs the question…

How should investors think about the value unlock opportunity?

RMH’s net asset value (NAV) as at 30 September 2023 was 104 cents per share. The current share price is 65 cents. This discount to NAV reflects a few important things:

- Bird in the hand: the market tends to apply some conservatism to management’s view on NAV until the cash is actually in the bank;

- Time until unlock: there is no certainty around how long the value unlock will take and time is literally money in the world of investing; and

- Perhaps most importantly: there may not be a buyer for all the assets!

That final point cannot be stressed enough. For example, who is going to buy the large minority stake in Atterbury? It’s really not obvious that these assets are easy to sell, otherwise it would’ve happened already. There’s every chance that we are a long way off RMH being able to shut down and return everything to shareholders.

In the meantime, returns will be driven by (1) conversion of the property NAV into cold, hard cash to the greatest extent possible and (2) the underlying movement in NAV i.e. the return achieved by the properties.

RMH may be following an unusual strategy with the kind of language that you won’t see in a company that intends to exist into perpetuity, but that doesn’t mean that the company isn’t exposed to the same opportunities and risks as other property groups. Concepts like funding costs and capitalisation rates for property valuations are relevant here. In an environment where interest rates start to come down, one would expect the RMH portfolio to do relatively well. There are some difficult property exposures in the portfolio though, so don’t treat this as a certainty.

My view: the way forward won’t be easy

The pro-forma NAV per share after the special distribution is 80.5 cents. Assuming the share price drops by the gross amount of the dividend, we are looking at a pro-forma price of 41.5 cents. That puts RMH on a post-dividend discount to NAV of 48.4%.

It’s not obvious that the NAV-to-cash magic is going to happen anytime soon, so it’s probably prudent to assume that you could be waiting a long time for the discount to close. This means that the discount needs to look reasonable vs. other property funds. There’s no shortage of property opportunities on the JSE at similar discounts that have far more coherent underlying portfolios, so RMH isn’t a bargain on that basis.

Value unlocks can work very well when there’s a clear path to unlocking the value. When the remaining assets are difficult to sell, investors can easily end up disappointed. As always, it comes down to understanding the opportunity vs. the risks and sizing any position accordingly.

As a final point, remember that as an individual shareholder buying the shares before the ex-dividend date, you’re most likely going to suffer a loss equal to the dividend withholding tax as the share price settles. This is because the gross dividend is still in the price, but you’ll only receive the net dividend.

Want to know more about the latest research?

Any opinions, news, research, reports, analyses, prices, or other information contained within this research is provided by an external contributor as general market commentary and does not constitute investment advice for the purposes of the Financial Advisory and Intermediary Services Act, 2002. First World Trader (Pty) Ltd t/a EasyEquities (“EasyEquities”) does not warrant the correctness, accuracy, timeliness, reliability or completeness of any information (i) contained within this research and (ii) received from third party data providers. You must rely solely upon your own judgment in all aspects of your investment and/or trading decisions and all investments and/or trades are made at your own risk. EasyEquities (including any of their employees) will not accept any liability for any direct or indirect loss or damage, including without limitation, any loss of profit, which may arise directly or indirectly from use of or reliance on the market commentary. The content contained within is subject to change at any time without notice.

Search all articles

Posts by topic

- Market News & Events

- Easy Community

- Education

- Dividends Update

- Exchange Traded Funds (ETFs)

- Property Investing

- Managed Bundles

- USD Wallet

- Retirement Annuity (RA)

- Cryptocurrency

- Tax Free Savings Account (TFSA)

- International Investing

- Unit Trusts

- New to Investing

- Artificial Intelligence

- EasyProtect

- EasyCredit

- Shares

- Government Bonds

- New Listings