Our Chief Investment Officer, Duane Gilbert, advises a cautious investment approach, favoring defensive US equities and global bonds for recession protection. It views South African equities as undervalued but risky, focusing on companies expected to perform well in a low-growth environment. The RISE portfolio includes high-yield South African Bonds, commodity-backed loans, and significant cash reserves, with a preference for the US dollar over the South African rand. This strategy, influenced by the rand's instability in 2023, positions the firm to capitalize on market opportunities.

Global Markets

The global equity rally continued in February, with nearly all major regions posting positive returns. US equities ended the month up 5.34% USD, European equities up 1.57%, Japanese equities up 8.39% and emerging markets up 4.76%. Chinese equities had a particularly strong month on the back of stimulus (up 8.39%). Chinese officials are now using the country’s sovereign wealth fund to buy shares to reverse a 3- year long market sell off. In addition, authorities introduced new regulations that require major institutional investors to buy more shares than they sell by the close of the trading day. The accounts of the country’s largest quant fund (Ningbo Lingjun Investment Management) were frozen for a few days for dumping local stocks. As one would expect, equity prices were supported by this buying, but it did nothing to improve the Chinese economic outlook. Chinese officials remain unwilling to use deficit spending for economic stimulus, which they believe would aggravate the structural imbalances that they are trying to address, and negatively impact long-term growth.

Chart 1: MSCI China vs MSCI World

Source: InFront

In the US, stock market gains continue to be driven by technology shares, which are benefitting from the excitement around artificial intelligence. After delivering 43.4% in 2023, the tech-heavy Nasdaq composite delivered 8% year-to-date. US tech stocks could very well dominate market returns in 2024 but are vulnerable to a market sell-off given their stretched valuations. 90% of the companies in the S&P 500 have now reported their Q4 2023 earnings with over three quarters beating expectation (source: FactSet). The magnificent 7 (Amazon, Apple, Microsoft, Nvidia, Google, Facebook and Tesla) have all met or exceeded expectations.

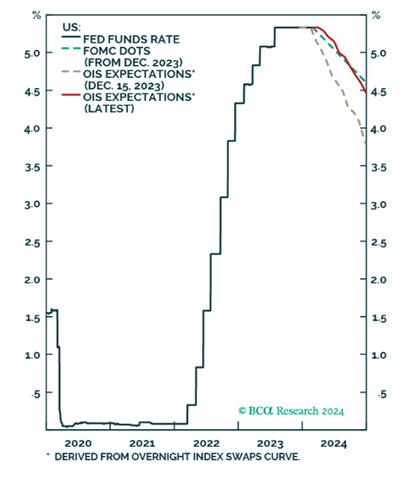

In contrast to equity markets, global bonds ended the month down 1.3%, as a higher-than-expected US inflation print led market participants to temper their expectations for rapid interest rate cuts.

Chart 2: Nasdaq vs S&P 500

Source: InFront

Chart 3: Markets are no longer pricing in more interest rate cuts than the Fed’s guidance (Source: BCA Research)

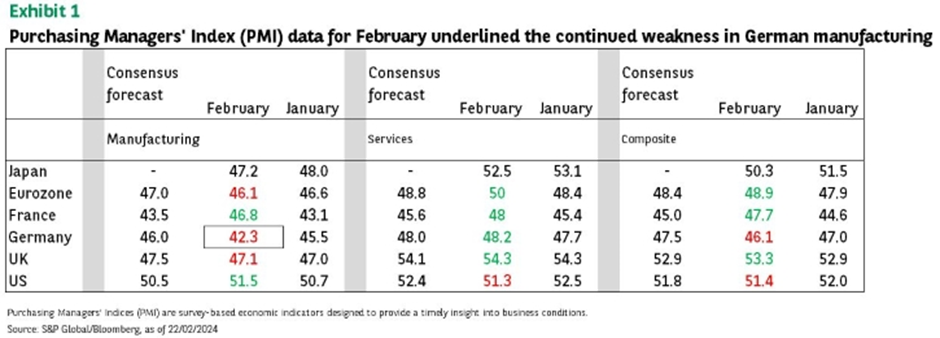

Economic data out of Europe was largely positive, which supported their markets. The composite eurozone PMI increased to an 8-month high of 48.9 in February (47.9 in January), suggesting that the downturn in the region is slowing. Services activity is now normalising, offsetting a sharp decline in manufacturing, particularly in Germany. While there has been some encouraging data releases this year, most indicators are still pointing towards further contraction in the region.

Chart 4: Eurozone PMI (Source: S&P Global/ Bloomberg)

Local Markets

Local markets were red across the board. The JSE All Share Index ended the month down 2.4% in ZAR, with the Resources 10 Index down 7.2%, the Financials 15 Index down 0.8% and the Industrial 25 Index down 0.6%. The Resources 10 Index is now down 20.4% over 1-year, highlighting how dependent the sector is on Chinese growth and demand. The standout performer for the month was multi-choice, after French media company, Canal+, made an offer to buy out shareholders at R105 a share (increased to R125 a share in March).

The JSE All Bond Composite lost 0.6% for the month and the composite inflation-linked bond index lost 0.7%. The rand lost 3.1% to the dollar and 2.8% to the Euro.

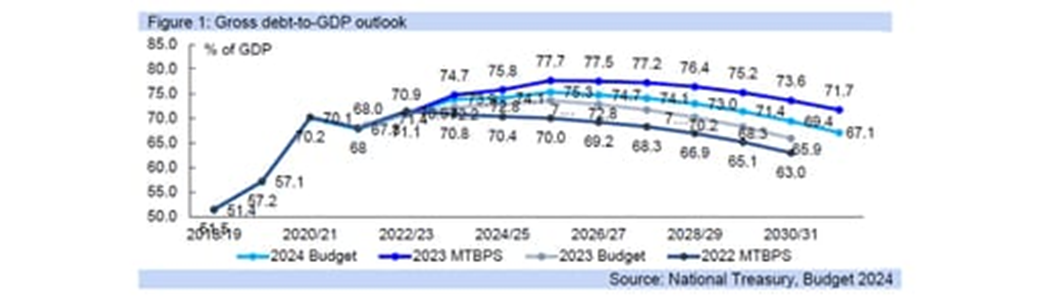

In economic news, Finance Minister Enoch Godongwana delivered the 2024 Budget on 21 February. Most notably, the treasury will draw R150bn from the country’s gold and foreign exchange contingency reserve account (GFECRA) over the next two years, to reduce the budget deficit and bring down the country’s borrowing costs. The total GFECRA stands at R500bn, and in the future, the Treasury is expected to draw on these reserves further.

Chart 6: Debt to GDP outlook (Source: National Treasury)

The Treasury also delivered an update on the two-pot retirement reform. Effective 1 September 2024, retirement contributions will be split one-third “savings pot” and two-thirds “retirement pot”. Members will be able to access their saving pot once year. Drawdowns will be taxed at your marginal rate. VAT and income taxes remain unchanged. Sin taxes on alcohol and tobacco rose between 6.7% and 7.2%, and between 4.7% and 8.2% respectively.

Commentary from our Chief Investment Officer, Duane Gilbert’s

Our market outlook for HY1 2024 is more bullish than it was in 2023. Falling inflation will give the Federal Reserve scope to cut interest rates, which will be supportive of equity markets (and bond markets to a lesser degree).

However, we should not forget that the recent interest rate hiking cycle was the most aggressive in 40 years, at a time where growth was already fragile. It is likely that the US will experience a mild recession by mid-year. A recession is also likely in Europe, and China seems likely to continue on its low growth trajectory in the absence of a meaningful stimulus package from the government.

As a result, we remain conservatively positioned in our portfolios, but with a tactical overweight to defensive US equities. We have a high allocation to global bonds which provide a strong hedge during a recession. South African equities are particularly cheap but vulnerable to a global sell-off. One needs to carefully pick companies that can grow their earnings in a low growth environment. Our portfolios have a high allocation to SA Bonds (where longer-dated instruments are still offering double-digit yields) and exposure to commodity backed loans. We also hold a lot of cash in our portfolios. We prefer USD over ZAR. The weakness we saw in 2023 despite a supportive global backdrop is testament to how fragile the ZAR is. Our large cash position gives us the dry powder we need to take advantage of bargains that may arise from a market sell-off.

Want to know more about the latest news?

Any opinions, news, research, reports, analyses, prices, or other information contained within this research is provided by an external contributor as general market commentary and does not constitute investment advice for the purposes of the Financial Advisory and Intermediary Services Act, 2002. First World Trader (Pty) Ltd t/a EasyEquities (“EasyEquities”) does not warrant the correctness, accuracy, timeliness, reliability or completeness of any information (i) contained within this research and (ii) received from third party data providers. You must rely solely upon your own judgment in all aspects of your investment and/or trading decisions and all investments and/or trades are made at your own risk. EasyEquities (including any of their employees) will not accept any liability for any direct or indirect loss or damage, including without limitation, any loss of profit, which may arise directly or indirectly from use of or reliance on the market commentary. The content contained within is subject to change at any time without notice.

Search all articles

Posts by topic

- Market News & Events

- Easy Community

- Education

- Dividends Update

- Exchange Traded Funds (ETFs)

- Property Investing

- Managed Bundles

- USD Wallet

- Retirement Annuity (RA)

- Cryptocurrency

- Tax Free Savings Account (TFSA)

- International Investing

- Unit Trusts

- New to Investing

- Artificial Intelligence

- EasyProtect

- EasyCredit

- Shares

- Government Bonds

- New Listings