The Finance Ghost attended a rather interesting venture capital conference in the past week. It was hosted by South African venture capital group Holocene and focused on what is known as ClimateTech – the various technologies aimed at reducing carbon emissions. In the keynote speeches, a fascinating comment was made about how FinTech used to attract vastly more investment than ClimateTech in South Africa. By 2023, this situation had changed to the point where they received roughly equal amounts of investment. In 2024, one would reasonably expect ClimateTech to pull ahead. Now, on one hand, this tells us that there is increased focus on carbon solutions and the environment at large. On the other, it tells us that FinTech has lost some of its shine. In explaining why the Finance Ghost plans to keep Visa and Mastercard as key positions in their portfolio, they'll be focusing on the latter. The Finance Ghost just thought you might find the former interesting as well, particularly as we can always learn a thing or two from capital flows in the venture capital game.

Payments businesses struggle to make money. The technology is expensive, the fraud risks are significant and substantial scale is required before there is any real hope of making a profit. They have to work extremely hard to achieve merchant adoption, without which there is no business at all. Even if they can convince merchants to accept them as a payment method, they also need to convince consumers to deviate from the numerous other methods to try this particular one.

And for what exactly, at the end of the day? Other than exceptions like buy-now-pay-later (which seems to be doing better in South Africa in terms of profitability than in the US, by the way), most of these solutions offer little in the way of benefits for the consumer.

You might assume that as online shopping has grown in popularity, the profits of FinTech groups have moved higher. Sadly, what tends to happen is that the bigger they get, the more money they lose. In the US, they try to hide this by using loads of stock-based compensation instead of cash payments to staff. This gets reversed out in the calculation of “adjusted EBITDA” – an absolutely nonsensical number that sadly found mass adoption amongst growth investors.

Don’t fall for it. The only numbers that matter in the US are GAAP (Generally Accepted Accounting Principles) numbers, which recognise stock-based compensation as an expense.

Pandemic heroes

The market was willing to bet on the FinTech story during the pandemic, when money was basically free and consumer spending was being stimulated like crazy by the Fed. In the aftermath of the pandemic, investors bailed.

The Global X FinTech ETF counts the likes of PayPal, Block (previously Square) and Adyen (a Dutch payments company) amongst its largest holdings. Fiserv is also in there, with various solutions including mobile banking. Over five years, this hasn’t proven to be an appealing investment at all:

Aside from the overall lack of through-the-cycle returns, take note of the extent of the volatility. Remember, a core principle in finance is that more risk must lead to more reward. There’s a whole lotta risk on that chart and not much reward.

On rails: owning the backbone of this ecosystem

The incredible thing about the global payments industry is that even the FinTech providers inevitably need to touch a Visa or Mastercard network at some stage of the journey. This network is known as the “payment rails” on which money effectively travels.

You can think of those rails as the national roads. Sure, it might be possible to travel short distances without climbing on a road starting with an N, but if you really want to get from one town to another, you have little choice. The alternative routes are much longer and usually unreliable. In the payments industry, there usually aren’t even any alternatives for longer trips.

An example of a trip that needs these rails? We don’t even need to use the obvious example of swiping a Visa or Mastercard branded card. Instead, we can consider paying for goods at a merchant using some kind of eWallet. The eWallet might have a lovely FinTech name, but the money can’t get to the merchant without travelling over the rails that the merchant is using. Ka-ching! That means money for Visa and/or Mastercard. In fact, the only time that this wouldn’t be the case is an eWallet-to-eWallet transaction of some kind.

And how often does that happen?

The beauty of Visa and Mastercard is that they have created an unassailable advantage over decades. Thanks to a vast network of merchants and card holders, the power of these businesses lies in their sheer scale. Cute little FinTechs may come and go, but inevitably they have to use a portion of the Visa or Mastercard network and pay for the privilege.

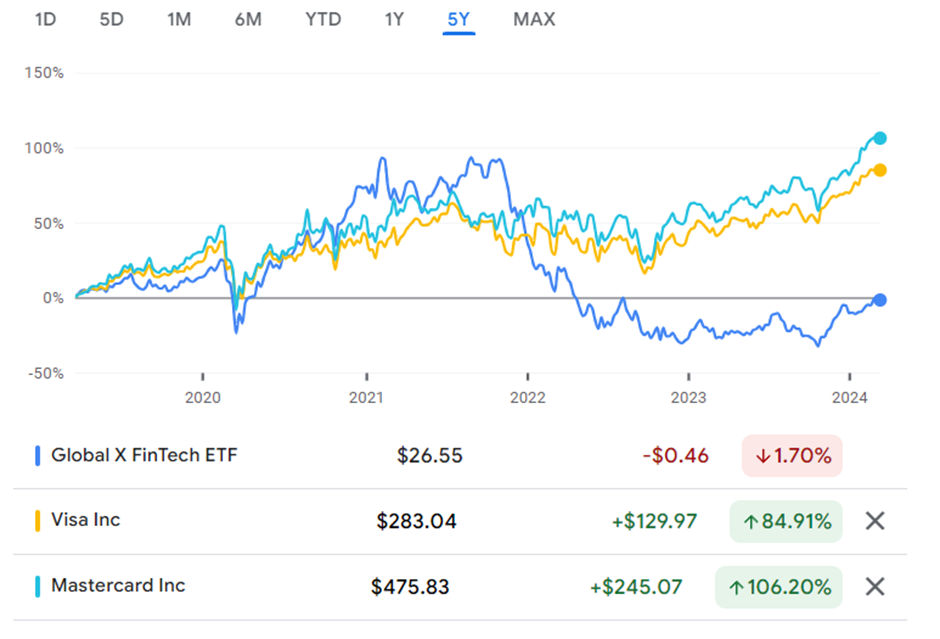

What does that look like on a share price chart? Well, here’s the Global X FinTech ETF once more, this time charted against Visa and Mastercard:

You don’t need to get the microscope out to spot the winners there. The backbone technology has absolutely smashed the new-and-exciting FinTechs over the past five years.

Will this situation change? Well, for as long as banks want to provide reliable card products to consumers, they will need to keep partnering with respected names like Visa and Mastercard. For as long as merchants want to have successful businesses, they will need to accept card payments from these two types of cards at the very least.

Even American Express hasn’t managed to achieve widespread acceptance at merchants. If you’ve ever had an American Express card, you’ll know that “do you take American Express?” becomes a core part of your vocabulary.

And the best part? Visa and Mastercard take absolutely no credit risk. Nothing. Nada. The banks take the credit risk. Visa and Mastercard simply supply the shovels in the ultimate gold rush: people needing to move money from A to B.

To disrupt these businesses, there would need to be mass global adoption of an entirely new money technology. Crypto enthusiasts would obviously love to jump in here. My view is that much like the other FinTech solutions, even crypto transactions will need to go back into the banking system at some stage. It’s simply not realistic to think that every consumer and merchant will suddenly start trusting a new blockchain technology. Even if they do, I’m not betting against Visa and Mastercard finding a way to participate in that value chain.

I sleep very easily at night with these names in my portfolio. Rather than trying to pick the winner, I simply bought both of them in equal measure. So far, so good.

Want to know more about the latest news?

Any opinions, news, research, reports, analyses, prices, or other information contained within this research is provided by an external contributor as general market commentary and does not constitute investment advice for the purposes of the Financial Advisory and Intermediary Services Act, 2002. First World Trader (Pty) Ltd t/a EasyEquities (“EasyEquities”) does not warrant the correctness, accuracy, timeliness, reliability or completeness of any information (i) contained within this research and (ii) received from third party data providers. You must rely solely upon your own judgment in all aspects of your investment and/or trading decisions and all investments and/or trades are made at your own risk. EasyEquities (including any of their employees) will not accept any liability for any direct or indirect loss or damage, including without limitation, any loss of profit, which may arise directly or indirectly from use of or reliance on the market commentary. The content contained within is subject to change at any time without notice.

Search all articles

Posts by topic

- Market News & Events

- Easy Community

- Education

- Dividends Update

- Exchange Traded Funds (ETFs)

- Property Investing

- Managed Bundles

- USD Wallet

- Retirement Annuity (RA)

- Cryptocurrency

- Tax Free Savings Account (TFSA)

- International Investing

- Unit Trusts

- New to Investing

- Artificial Intelligence

- EasyProtect

- EasyCredit

- Shares

- Government Bonds

- New Listings