In January 2024, the market witnessed a series of significant events. Our Chief Investment Officer, Duane Gilbert, provides valuable insights into these developments. RISE maintains a cautious approach, strategically favoring defensive US equities and placing a significant emphasis on global bonds. While South African equities present an attractive opportunity due to their affordability, they are also exposed to vulnerability.

Global Markets

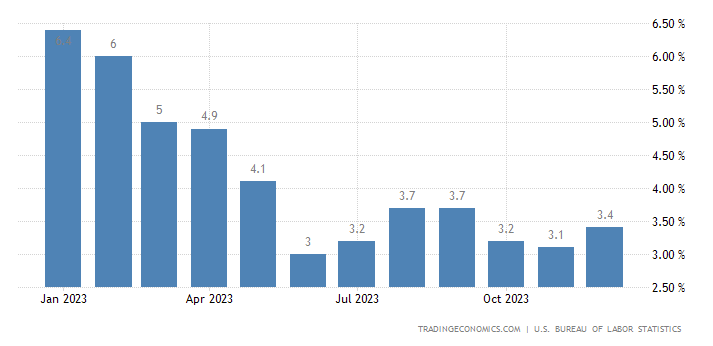

Global equity markets were up only slightly in January after staging a strong rally in the last two months of 2023. As we discussed in previous commentaries, the over riding bullish theme of 2023 was falling US inflation and the expectations that the US Federal Reserve will be able to cut interest rates “soon”. This theme strengthened in December after another low US inflation print led the Fed to acknowledge that the reversal in inflation trends could spark a resumption in interest rate cuts. This theme seems to have peaked after Powell stated that the Fed will move carefully on rate cuts, with probably fewer than the market expects.

Chart 1: US Inflation close to Fed’s 2% target (Source: Trading Economics)

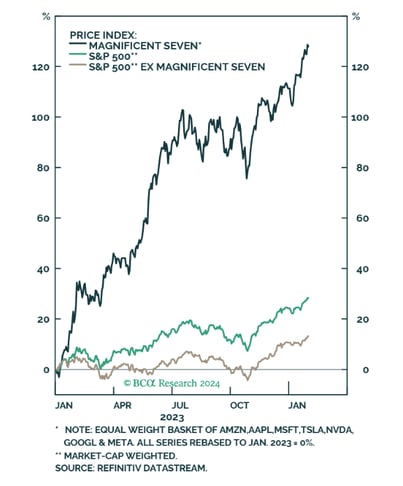

The MSCI World ended the month up 1.2%, with US equities up 1.6% and European equities down 0.1%. While we did touch on it in last month’s commentary, it’s worth mentioning again that equity market returns are largely driven by large cap tech stocks, in particular, Amazon, Apple Alphabet (Google), Microsoft, Meta (Facebook), Tesla and Nvidia. These stocks have been dubbed the ‘Magnificent 7’ and have been the main beneficiaries of the artificial intelligence excitement. However, Tesla gave back most of its gain in January, losing 24.6% for the month, and the media phrase is quickly changing to the ‘Magnificent 6’.

Chart 2: Performance of US large-cap Tech Stocks (Source: BCA Research)

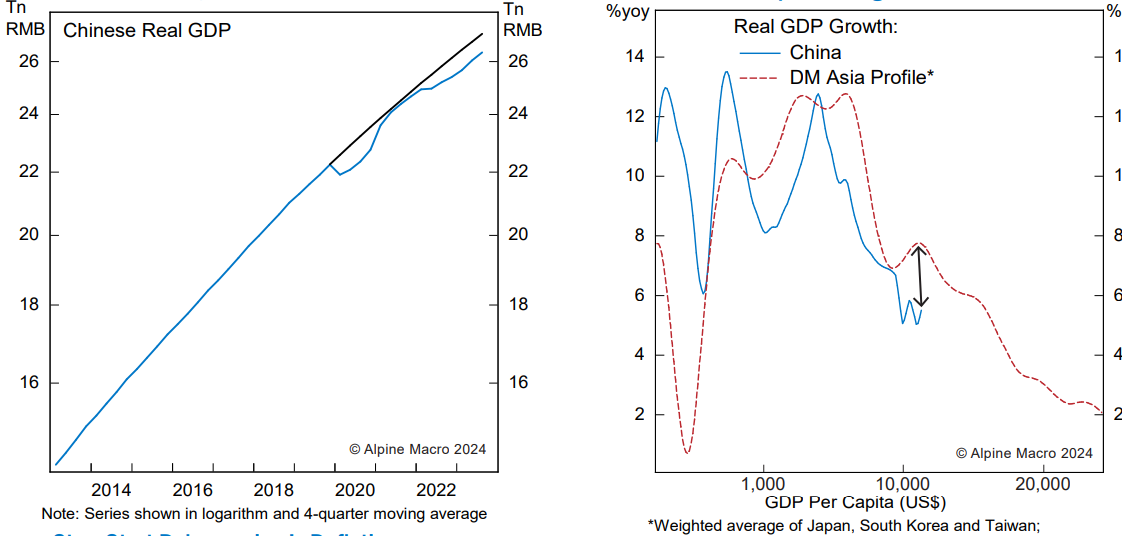

Chinese equities continued to disappoint in January, with the MSCI China index down 10.6%. In last month’s commentary we discussed how Chinese growth is under pressure as a result of destructive policies targeting the property, technology, private education/healthcare and other sectors, which are aimed at reinforcing the government’s control over the private sector and redistributing wealth. In January, the People’s Bank of China announced stimulus in the form of smaller cash reserves and increased lending to property developers. This is too little, too late, and the ongoing underperformance of the Chinese equity markets highlights that investors do not expect meaningful stimulus from the government. Industrial metals and the currencies of commodity exporting emerging markets also fell in response to the announcement.

Chart 3: Chinese growth is below trend and underperforming other Asian markets (Source Alpine Macro)

Local Markets

Local markets were hit hard by the negative stimulus announcement from China. The JSE All Share Index ended the month down 2.9%. As one would expect, the resources Index was the biggest loser, down 5.9%, While financials and industrials lost 2.9% and 1.3% respectively. the rand ended the month at 18.67 to the dollar, after briefly touching 18.30 earlier in the month. It has become clear that the positivity that global developed markets have experienced is not spilling over into emerging markets, as we suggested could be the case in last month’s commentary. This is largely due to concerns around China as well as domestic issues.

The JSE All Bond Composite gained 0.7% for the month and the composite inflation-linked bond index gained 0.1%. Annual consumer price inflation pulled back in December, easing to 5.1% year-on-year from 5.5% in November. This allowed the SARB to keep the repo rate steady at 8.25%.

Chief Investment Officer, Duane Gilbert’s Commentary

Our market outlook for HY1 2024 is more bullish than it was in 2023. Falling inflation will give the Federal Reserve scope to cut interest rates, which will be supportive of equity markets (and bond markets to a lesser degree). However, we should not forget that the recent interest rate hiking cycle was the most aggressive in 40 years, at a time where growth was already fragile. It is likely that the US will experience a mild recession by mid-year. A recession is also likely in Europe, and China seems likely to continue on its low growth trajectory in the absence of a meaningful stimulus package from the government.

As a result, we remain conservatively positioned in our portfolios, but with a tactical overweight to defensive US equities. We have a high allocation to global bonds which provides a strong hedge during a recession. South African equities are particularly cheap but vulnerable to a global sell-off. One needs to carefully pick companies that can grow their earnings in a low growth environment. Our portfolios have a high allocation to SA Bonds (where longer-dated instruments are still offering double-digit yields) and exposure to commodity backed loans. We also hold a lot of cash in our portfolios. We prefer USD over ZAR. The weakness we saw in 2023 despite a supportive global backdrop is testament to how fragile the ZAR is. Our large cash position gives us the dry powder we need to take advantage of bargains that may arise from a market sell-off.

Any opinions, news, research, reports, analyses, prices, or other information contained within this research is provided by an employee of EasyEquities an authorised FSP (FSP no 22588) as general market commentary and does not constitute investment advice for the purposes of the Financial Advisory and Intermediary Services Act, 2002. First World Trader (Pty) Ltd t/a EasyEquities (“EasyEquities”) does not warrant the correctness, accuracy, timeliness, reliability or completeness of any information (i) contained within this research and (ii) received from third party data providers. You must rely solely upon your own judgment in all aspects of your investment and/or trading decisions and all investments and/or trades are made at your own risk. EasyEquities (including any of their employees) will not accept any liability for any direct or indirect loss or damage, including without limitation, any loss of profit, which may arise directly or indirectly from use of or reliance on the market commentary. The content contained within is subject to change at any time without notice.

Search all articles

Posts by topic

- Market News & Events

- Easy Community

- Education

- Dividends Update

- Exchange Traded Funds (ETFs)

- Property Investing

- Managed Bundles

- USD Wallet

- Retirement Annuity (RA)

- Cryptocurrency

- Tax Free Savings Account (TFSA)

- International Investing

- Unit Trusts

- New to Investing

- Artificial Intelligence

- EasyProtect

- EasyCredit

- Shares

- Government Bonds

- New Listings