The Finance Ghost shares his excitement about Microsoft, a tech giant that has really blown people away. Why is Microsoft so interesting? Between 2006 and 2023, its value shot up almost ten times - that's huge! In this piece, we'll take a closer look at what Microsoft did to achieve such success and how it's managed to keep going strong even when times got tough.

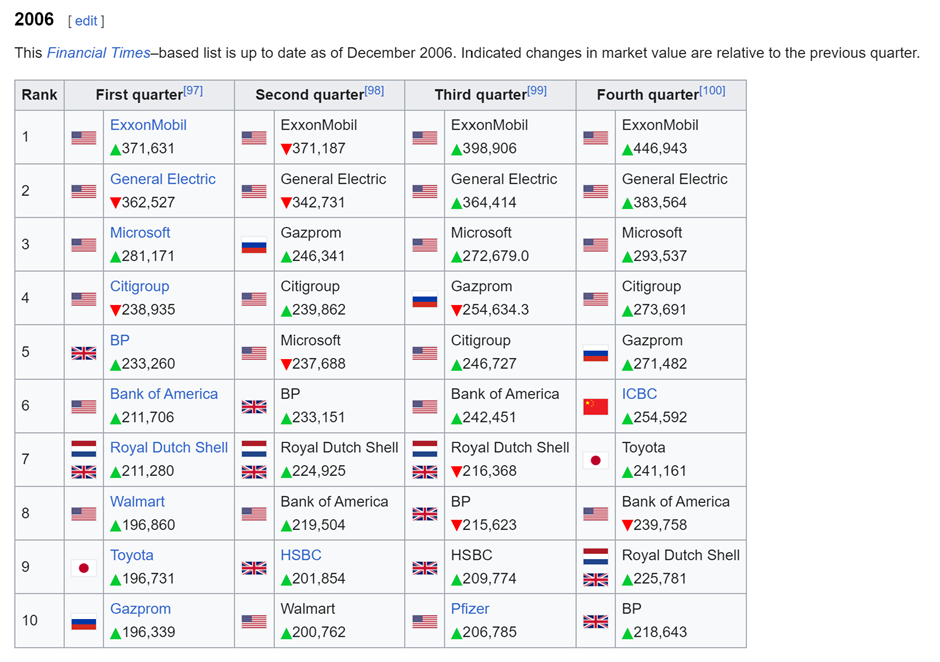

Do yourself a favour and search for the top ten most valuable companies in the world in the “Big Oil” era. Better yet, just look at the table below from Wikipedia, because I’ve done the hard work for you:

Oil companies, industrials, retailers, banks and… Microsoft. There it is, solidly top five. Now let’s take a look at the 2003 list, also off Wikipedia:

What do you notice? Yup, the only company that features in both lists is Microsoft, a company that has increased its market cap by a factor of nearly 10x between 2006 and 2023. I should remind you that this period included the Global Financial Crisis (GFC) and of course the joys of COVID. Microsoft’s staying power cannot be disputed. Best of all, to stay around in the top ten list, it means there is plenty of growth. You can’t go sideways and maintain this status (evidenced by ExxonMobil’s 2006 market cap being lower than the tenth placed company in 2023).

You should also take note that there isn’t a single company in the top ten that is a big oil or industrials player. Also, the only non-US company in the list is Taiwan Semiconductor Company. You win no prizes for guessing (1) where the company is based and (2) what they manufacture.

US tech has been the runaway success story in the post-GFC era. Rather than suffering at the hands of COVID, the pandemic actually gave this entire industry a strong boost. Remote working and cloud computing products were accelerated rather than negatively impacted.

It’s really as simple as this: Microsoft is my favourite company. It’s the one I would choose if I could only choose one. But why am I so firmly a believer in Satya Nadella (the CEO) and the strategy at Microsoft?

Exceptional moats

Microsoft is a collection of excellent and very good businesses, with the devices business as the only blemish on the story. I’m genuinely not sure why they bother with manufacturing devices and I wish they would stop. The less said about that, the better. It’s thankfully just a small distraction anyway.

Moving on to the real value drivers, it’s very unlikely that you go a single day without touching a Microsoft product. Even if you work on Google Workspace for word processing and spreadsheets, you probably still have a LinkedIn profile. Guess what? That’s owned by Microsoft. When you go home and relax with an Xbox, that’s also Microsoft.

Is Artificial Intelligence (AI) starting to have an impact on your life, positively or negatively? Chat GPT is also part of the Microsoft story. They do a spectacularly good job of positioning themselves for important trends, usually far up the value chain.

Cloud computing is the perfect example, which is what the past decade at Microsoft will be remembered for. As the world moved from buying software in stores to paying for recurring subscriptions online, Microsoft was there to make a profit.

There are a vast number of users of Office 365 products, which means a beautiful recurring revenue base that is hardly price sensitive. To shift a significant organisation to Google Workspace is a big decision and not one that you’ll see very often. This gives Microsoft pricing power and the ability to access the world’s most impressive commercial audience for new product launches.

Case in point: the way in which Teams obliterated the Zoom growth story. Just take a look at the Zoom share price over the past five years vs. Microsoft:

At the very top of the cloud value chain, we find the technology that powers the infrastructure. Microsoft’s Azure product benefits from the distribution power of Office 365 (and other productivity tools), making it a natural choice for companies that are already using Microsoft products. Amazon’s AWS is a formidable competitor, but also in very different ways. There are others playing in that space as well, like Google.

The thing to remember about Microsoft is that it doesn’t have one particular strength in the market that gives it a strong position, like Adobe for example, or Salesforce. Instead, it touches almost every element of modern computing, ranging from productivity tools to cloud and gaming.

And social media, of course. Don’t understand how good a business LinkedIn is. You’ll be #humbled by it.

What do the latest numbers say?

More of the same really. There’s growth – lots of growth!

Microsoft Cloud grew by 24% in the latest quarter. The sheer scale of that number is ridiculous, as this is a business doing more than $33 billion in revenue that is still growing like an early stage company. They are talking about “infusing AI at every layer of the tech stack” and it’s clearly working, with over half of the Fortune 500 companies using Azure OpenAI today.

The clear trend is that spend is going to shift from other expense lines (like staff costs) into cloud productivity, as companies increasingly use AI to make employees more productive. Data stored in Microsoft Fabric’s data lake increased 46% quarter-over-quarter i.e. in the space of just three months!

There’s record usage at Teams, with more than two-thirds of enterprise Teams customers buying Phone, Rooms or Premium. There are more than 400 million paid Office 365 seats, giving Microsoft exceptional distribution power for products. This is the point I made previously about what happened to Zoom.

The list just goes on and on. Even Windows has an exciting story to tell, with the addition of the Copilot Key. Microsoft calls this the first significant change to Windows Keyboard in more than 30 years!

At LinkedIn, there are 1 billion members. That’s astonishing. There’s not a better professional database anywhere in the world.

In gaming, even though Microsoft is executing job cuts to achieve some of the synergies required to make the ActivisionBlizzard acquisition as success, there’s strong growth in streaming and of course they now have a much bigger business as a platform going forward.

With all said and done, revenue was up 16% in constant currency and operating income grew 23% (also in constant currency). Earnings per share also increased by 23% in constant currency. Results were ahead of expectations, reminding me once more why I love this company.

No free lunches

Microsoft isn’t exactly a hidden gem on the market. You certainly aren’t in value stock territory. This is firmly in a quality and growth theme, which means lofty valuation multiples.

A sales multiple of 13x is usually enough to make me run as far as possible in the other direction. Microsoft is a high margin business though, so what seems like an obscene sales multiple actually translates into a Price/Earnings multiple of 36.5x. That’s still high of course, but it’s not completely absurd.

At a 23% growth rate in earnings and with such deep moats, Microsoft’s valuation isn’t enough to make me walk away. Volatility along the way is a guarantee rather than a risk, serving up opportunities to buy the dip.

In my opinion, Microsoft is still going to be in the top ten market cap list in ten years from now. In fact, I suspect it will sit proudly at the top of the list.

Want to know more about the latest news?

Any opinions, news, research, reports, analyses, prices, or other information contained within this research is provided by an external contributor as general market commentary and does not constitute investment advice for the purposes of the Financial Advisory and Intermediary Services Act, 2002. First World Trader (Pty) Ltd t/a EasyEquities (“EasyEquities”) does not warrant the correctness, accuracy, timeliness, reliability or completeness of any information (i) contained within this research and (ii) received from third party data providers. You must rely solely upon your own judgment in all aspects of your investment and/or trading decisions and all investments and/or trades are made at your own risk. EasyEquities (including any of their employees) will not accept any liability for any direct or indirect loss or damage, including without limitation, any loss of profit, which may arise directly or indirectly from use of or reliance on the market commentary. The content contained within is subject to change at any time without notice.

Search all articles

Posts by topic

- Market News & Events

- Easy Community

- Education

- Dividends Update

- Exchange Traded Funds (ETFs)

- Property Investing

- Managed Bundles

- USD Wallet

- Retirement Annuity (RA)

- Cryptocurrency

- Tax Free Savings Account (TFSA)

- International Investing

- Unit Trusts

- New to Investing

- Artificial Intelligence

- EasyProtect

- EasyCredit

- Shares

- Government Bonds

- New Listings