Taking a look at what happened in the markets in July 2023.

Taking a look at the Global Markets

July 2023 was yet another good month for global equities as falling global inflation fueled hopes for a soft landing (a slowdown where a recession is avoided). The MSCI (developed) World ended the month up 3.4% in USD. Developed market equities are now close to their all-time highs reached when monetary stimulus was at its peak (post-covid) suggesting that by and large, the market believes a global recession will be avoided. The key data print in this regard was US inflation, which slowed to 3% in June after peaking at 9.1% just 12 months ago. US core inflation remained stickier at 4.8%.

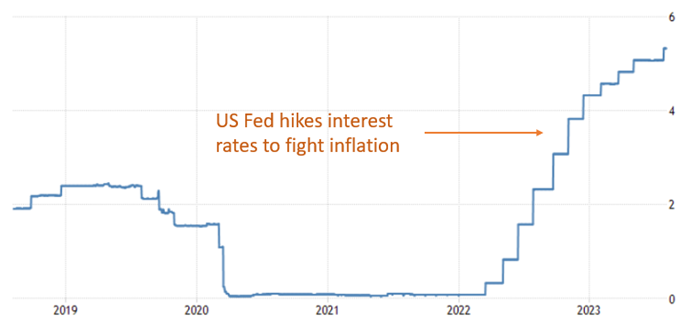

Also supporting markets in July was a strong US Q2 GDP print of 2.4% vs 2.0% expected. Despite the slowdown in inflation and strong growth numbers, the Fed hiked rates by another 0.25% in July. The European Central Bank also raised rates by 0.25%, in line with guidance.

Chart 1: Developed Market Equities (Source: Infront)

Chart 2: US Interest Rates (Source: Trading Economics)

Emerging markets also had a good month in July (up 6.2% in USD), driven by expectation for stimulus from China after the Politburo vague promises about implementing macro adjustments in a “precise and forceful manner” but gave no details. Historically, Chinese stimulus programs have had a massive impact on global growth, particularly commodity-exporting emerging markets. However, high levels of debt, and a property bubble have taken away China’s ability to stimulate growth in recent years. Nevertheless, this is the first mention of stimulus in at least 12 months, and it caused a lot of excitement among emerging market investors.

Chart 3: China Stimulus vs Commodity Prices (Source: BCA)

Japanese equities ended the month up 3% as gains in USD were boosted by a stronger Yen, after the Bank of Japan loosened it’s yield curve control. The Bank of Japan will now allow 10- year bond yields to fluctuate slightly around their zero percent target level to enhance the sustainability of their yield curve control strategy, and buy 10 year government bonds at up to 1% through open market operations. On the fixed income side, global bonds ended the month up 0.4% in USD on falling inflation expectations and the prospect for interest rate cuts falling back into neutral territory, if a global recession is avoided. Commodities had a strong month across the board. The Bloomberg Commodity Index gained 6.3%. Oil was the largest gainer (Brent crude up 12.2%) on Saudi supply cuts and the prospect for higher global growth.

Taking a look at the Local Markets

Local markets took their direction from global markets, with the JSE All Share Index ending the month up 4% in ZAR. Gains were broad based; however, resources continue to underperform other sectors by more than 20% over 6-months. Notable movers for the month were SA inc. counters (banks, retailers, property shares etc) as a result of improving sentiment – US recession looks less inevitable, load shedding seems to be getting better, and Vladimir Putin has withdrawn from the upcoming BRICS summit in South Africa. The rand also benefitted from this improvement in sentiment, gaining 6.3% against the dollar and 4.3% against the Euro.

The JSE All Bond Composite gained 2.3% in July, supported by a pause in the interest rate hikes at the SARB’s Monetary Policy Committee meeting. Gains were led by the long end of the curve, which seems to be recovering from a prolonged period of negative sentiment. The composite inflation-linked bond index gained 1.4%. Annual consumer price inflation was 5.4% in June 2023. This is the first time in over a year that inflation is within the SARB’s 3-6% band. The high interest rates in South Africa are doing their job of bringing down inflation, which gave the SARB the leeway to pause interest rate hikes in July, a much needed break for the South African consumer. The repo rate now sits at 8.25%, making cash and money market instruments an attractive proposition to South African savers.

The 15th of July was the deadline for industry participants to provide comment on the revised two-pot legislation. Under the revised legislation, members will be allowed to access 10% of their existing retirement savings up to a maximum of R25 000. The first draft of the legislation only made provision for members to make future contributions into a “savings pot” (one third) and a “retirement pot” (two thirds). The “savings pot” will then be available for withdrawal before retirement. The ability to access the “savings pot” will be provided without the member having to cease employment. The implementation date for the two-pot regulation is 31 March 2024.

|

ON THE RISE |

|||||

|

Local Markets |

Month |

Year to Date |

1 Year |

3 Year |

5 Year |

|

SWIX |

4.1% |

8.2% |

15.4% |

13.2% |

7.1% |

|

Mid Cap |

5.8% |

4.5% |

9.0% |

15.7% |

6.3% |

|

Small Cap |

1.4% |

2.7% |

6.1% |

29.8% |

9.2% |

|

Industrial 25 |

2.8% |

22.0% |

32.7% |

15.6% |

10.2% |

|

Resources 10 |

3.7% |

-7.3% |

5.8% |

11.1% |

14.8% |

|

Financial 15 |

7.9% |

14.9% |

19.9% |

24.4% |

5.0% |

|

JSE All Bond Composite |

2.3% |

4.2% |

10.1% |

8.2% |

7.4% |

|

CILI |

1.4% |

1.7% |

4.2% |

9.7% |

5.6% |

|

STEFI |

0.7% |

4.4% |

7.1% |

5.1% |

5.8% |

|

Global Markets |

Month |

YTD |

1 Year |

3 Year |

5 Year |

|

S&P 500 |

3.1% |

19.5% |

11.1% |

11.9% |

10.3% |

|

MSCI Emerging Markets |

6.2% |

11.4% |

8.3% |

1.5% |

1.7% |

|

MSCI World |

3.4% |

19.0% |

13.5% |

11.7% |

9.1% |

|

MSCI Europe |

3.1% |

17.1% |

19.6% |

10.4% |

5.1% |

|

Commodities |

Month |

YTD |

1 Year |

3 Year |

5 Year |

|

Gold (Spot) |

2.4% |

7.7% |

11.2% |

-0.2% |

9.9% |

|

Platinum (Spot) |

5.5% |

-12.3% |

4.2% |

1.3% |

2.2% |

|

Brent Crude Oil (Spot) |

13.5% |

-0.9% |

-17.8% |

25.0% |

2.8% |

|

Exchange Rate |

Month |

YTD |

1 Year |

3 Year |

5 Year |

|

ZARUSD |

6.3% |

-4.1% |

-6.2% |

-1.4% |

-5.7% |

|

ZAREUR |

4.3% |

-7.4% |

-13.6% |

0.7% |

-4.7% |

|

ZARGBP |

3.9% |

-10.3% |

-11.7% |

-1.0% |

-5.4% |

Comments from our Chief Investment Officer, Duane Gilbert

With the downward trend in global inflation, markets are confident that a recession will be avoided. We feel this is unlikely given the aggressiveness of interest rate hikes, at a time where global growth is fragile. Even if a recession can be avoided, valuations are too sanguine given the rapid withdrawal of liquidity, low global growth and high geopolitical risks.

Fundamentally, the market environment remains unsupportive. As a result, we maintain a conservative positioning in our portfolios. Our exposure to global equities is low. Within equities we have taken a more defensive stance, favouring US quality equities and defensive sectors. We have a high allocation to global bonds which provide a strong hedge during a recession. South African equities are particularly cheap but vulnerable to a global sell-off. One needs to carefully pick companies that can grow their earnings in a low growth environment.

Our portfolios have a high allocation to SA Bonds (where longer-dated instruments are still offering double-digit yields) and exposure to commodity backed loans. We also hold a lot of cash in our portfolios. We prefer USD over ZAR given the recent rally in the rand and the countercyclical nature of the dollar. Our large cash position gives us the dry powder we need to take advantage of bargains that may arise from a market sell-off. Finally, we have a position in renewable energy infrastructure projects, which are not only attractive from an IRR perspective but will meaningfully increase electricity production and reduce carbon emissions in South Africa.

-2.png?width=1200&length=1200&name=image%20(10)-2.png)

Any opinions, news, research, reports, analyses, prices, or other information contained within this research is provided by an employee of EasyEquities an authorised FSP (FSP no 22588) as general market commentary and does not constitute investment advice for the purposes of the Financial Advisory and Intermediary Services Act, 2002. First World Trader (Pty) Ltd t/a EasyEquities (“EasyEquities”) does not warrant the correctness, accuracy, timeliness, reliability or completeness of any information (i) contained within this research and (ii) received from third party data providers. You must rely solely upon your own judgment in all aspects of your investment and/or trading decisions and all investments and/or trades are made at your own risk. EasyEquities (including any of their employees) will not accept any liability for any direct or indirect loss or damage, including without limitation, any loss of profit, which may arise directly or indirectly from use of or reliance on the market commentary. The content contained within is subject to change at any time without notice.

Search all articles

Posts by topic

- Market News & Events

- Easy Community

- Education

- Dividends Update

- Exchange Traded Funds (ETFs)

- Property Investing

- Managed Bundles

- USD Wallet

- Retirement Annuity (RA)

- Cryptocurrency

- Tax Free Savings Account (TFSA)

- International Investing

- Unit Trusts

- New to Investing

- Artificial Intelligence

- EasyProtect

- EasyCredit

- Shares

- Government Bonds

- New Listings