Taking a look at what happened in the markets in November 2023.

Global Markets

November saw a sharp rally in global equities after a low inflation print from the US fuelled expectations that inflation will fall below the US Federal Reserve’s 2% target soon, allowing the Fed to bring down interest rates and avoid a recession. Developed market ended the month up 9.4% in USD, with US equities up 9.4%, and European equities up 9.9%.

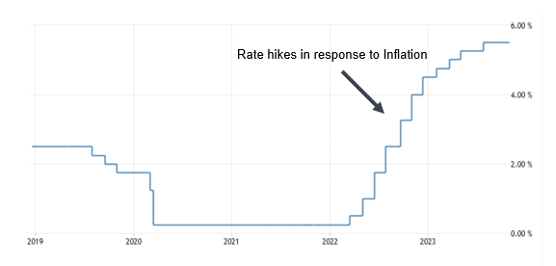

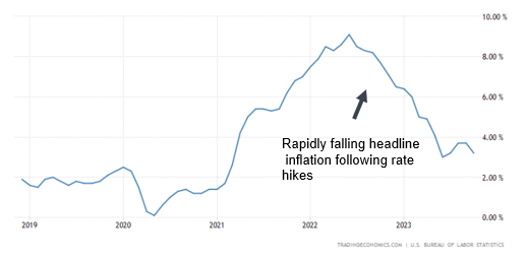

In March 2022, the Fed embarked on its most aggressive rate hiking cycle in 40 years in order to combat the inflationary impact of excessive spending during the Covid-19 pandemic. The interest rate hikes were remarkably effective. With US inflation falling from its peak of 9.1% year-on-year in July 2022 to 3.2% in October 2023. Markets expect inflation to keep this downward momentum and fall below the Fed’s target soon, and as a result, are pricing in interest rate cuts during the first half of 2024. High interest rates are a headwind to any economy and the current interest rates in the US will likely lead to a recession if sustained. The strong rally in Equity markets in November suggest that market consensus is now for a “recession avoided” scenario. Global Bonds also made strong gains in November with expectations for central banks to cut interest rates in HY1 2024. The Bloomberg Barclays Global aggregate Bond Index ended the month up 5.0% in USD.

Chart 1: US Interest Rates (Source: Trading Economics)

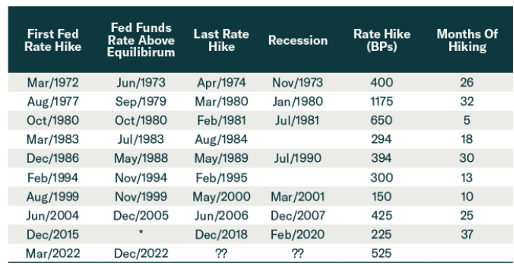

Chart 2: Comparison of current interest rate cycle to previous ones (Source: BCA Research)

Chart 3: US Inflation (Source: Trading Economics)

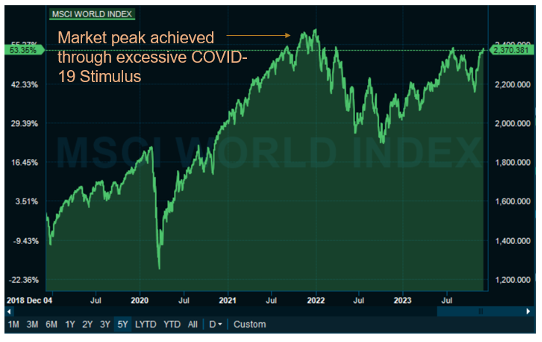

Chart 4: Developed Markets are now approaching all-time highs (Source: Infront)

Local Markets

Local markets took their direction from global markets, with the JSE All Share Index gaining 8.6% in ZAR. Gains were broad based, with the Resource 10 Index up 5.9% for the month, The Industrial 25 Index up 10.5%, and the Financial 15 Index up 8.7%.

The JSE All Bond Composite gained 4.8% in November. Gains were driven by the 7-12 year and 12-year+ segments of the yield curve suggesting that the country “risk-premium” improved after Finance Minister Enoch Godongwana delivered a conservative and well-balance Medium-Term budget Policy Statement. The composite inflation-linked bond index gained 4.8%. The high interest rates in South Africa are doing their job of bringing inflation within the SARB’s 3-6% target, which gave the SARB the leeway to hold-off interest rate hikes for a third consecutive meeting, a much needed break for the South African consumer. The repo rate now sits at 8.25%, making cash and money market instruments an attractive proposition to South African savers. Surprisingly, the rand did not benefit from the positive global and domestic environment. After a short-lived rally to 18.19 to the dollar, the ZAR quickly gave up its gains to close the month at 18.85 to the dollar.

Medium-Term Budget Policy Statement highlights:

- SA’s main budget deficit projected at of 4.9 per cent of GDP compared to previous estimate of 4.0 percent in February.

- The gross debt rises from R4.8 trillion in 2023/24 to R5.2 trillion in the next financial year. By 2025/26, it will exceed the R6 trillion mark.

- Over the next three years, debt-service costs as a share of revenue will increase from 20.7 per cent in 2023/24 to 22.1 per cent in 2026/27.

- In the current financial year, spending has been revised down by R21 billion. Further reductions of R64 billion in 2024/25 and R69 billion in 2025/26 are proposed.

- R34 billion is allocated to extend the Covid-19 Social Relief of Distress grant by another year.

- Additional funding of R24 billion this year and R74 billion over the medium term will be used to fund the 2023/24 wage increase and the associated carry-through costs in these sectors.

- Eskom Debt Relief Amendment Bill– reduction of the amount of debt relief available to Eskom, in the event that the entity does not comply with the National Treasury conditions. Requires payment of interest by Eskom on amounts advanced as part of the debt relief loan.

- Transnet Freight Logistics Roadmap - No further financial assistance to Transnet until the entity enhances efficiencies, facilitating the introduction of competition and leveraging the financial and technical support of the private sector.

Transnet Freight Logistics Roadmap - No further financial assistance to Transnet until the entity enhances efficiencies, facilitating the introduction of competition and leveraging the financial and technical support of the private sector.

Comments from our Chief Investment Officer, Duane Gilbert

Markets are bullish that the US Federal Reserves will cut interest rates early in 2024, and that a US recession will be avoided. This bullish sentiment is likely to continue driving markets into Q1 2024. However, we of the view that inflation remains sticky at these levels, and that the Fed is unlikely to cut rates any time soon.

We believe that a US recession is likely to play out in the first half of 2024, even if it is a mild recession. Recession aside, we believe that valuations are too sanguine given the rapid withdrawal of liquidity, low global growth and high geopolitical risks. Fundamentally, the market environment remains unsupportive. As a result, we maintain a conservative positioning in our portfolios. Our exposure to global equities is low. Within equities we have taken a more defensive stance, favouring US quality equities and defensive sectors. We have a high allocation to global bonds which provide a strong hedge during a recession. South African equities are particularly cheap but vulnerable to a global sell-off. One needs to carefully pick companies that can grow their earnings in a low growth environment.

Our portfolios have a high allocation to SA Bonds (where longer-dated instruments are still offering double-digit yields) and exposure to commodity backed loans. We also hold a lot of cash in our portfolios. We prefer USD over ZAR. The weakness we saw in November despite a supportive global and local backdrop is testament to how fragile the ZAR is. Our large cash position gives us the dry powder we need to take advantage of bargains that may arise from a market sell-off.

-2.png?width=1200&length=1200&name=image%20(10)-2.png)

Any opinions, news, research, reports, analyses, prices, or other information contained within this research is provided by an employee of EasyEquities an authorised FSP (FSP no 22588) as general market commentary and does not constitute investment advice for the purposes of the Financial Advisory and Intermediary Services Act, 2002. First World Trader (Pty) Ltd t/a EasyEquities (“EasyEquities”) does not warrant the correctness, accuracy, timeliness, reliability or completeness of any information (i) contained within this research and (ii) received from third party data providers. You must rely solely upon your own judgment in all aspects of your investment and/or trading decisions and all investments and/or trades are made at your own risk. EasyEquities (including any of their employees) will not accept any liability for any direct or indirect loss or damage, including without limitation, any loss of profit, which may arise directly or indirectly from use of or reliance on the market commentary. The content contained within is subject to change at any time without notice.

Search all articles

Posts by topic

- Market News & Events

- Easy Community

- Education

- Dividends Update

- Exchange Traded Funds (ETFs)

- Property Investing

- Managed Bundles

- USD Wallet

- Retirement Annuity (RA)

- Cryptocurrency

- Tax Free Savings Account (TFSA)

- International Investing

- Unit Trusts

- New to Investing

- Artificial Intelligence

- EasyProtect

- EasyCredit

- Shares

- Government Bonds

- New Listings