The Finance Ghost reflects on some of the initial ideas he had for Sasol and Zeda that were previously discussed on EasyEquities, emphasizing the importance of allowing time for these ideas to unfold and generate outcomes. Despite being relatively recent, it is intriguing to know they're playing out.

When you form a view on something, you should know that you have a pretty good chance of being completely wrong. If the markets were easy to predict, then everyone would make a fortune and nobody would care about the track record at Berkshire Hathaway.

Does this mean that you shouldn’t try? Of course not! Investing is like a magnificent jigsaw puzzle that never stops moving around. There’s new information literally every single day, which is why you have to constantly question your own thesis and adjust it where necessary.

When I write about stocks, this is exactly why I focus more on why I feel a certain way, rather than what I think the outcome might be. This is to give you clues as to what could change my mind in future. Although there are strong arguments for letting things run and allowing market volatility to sort itself out, I’m equally sure that nobody who holds in shares in Ellies is sitting there feeling good about not getting off the sinking ship.

With that in mind, it’s time to look back on some of the earlier ideas that I wrote on for EasyEquities and how they turned out. It’s important to give the market some time for an idea to work out (or not), otherwise the result is just noise rather than the outcome of sound analysis. Although these ideas are only a few months old, it’s interesting to see how they have played out.

Sasol: published 20 November 2023

I described Sasol as being “less broken” than it was at the start of the pandemic when investors piled in and took a bet on eyewatering potential returns. This doesn’t mean that things are going well, of course. It just means that the company isn’t trading at outrageously low levels.

I focused the article on what Sasol is really exposed to, particularly as the correlation with the oil price had broken down in recent times. Here’s how I ended the piece:

“In my opinion, it’s now in the “too hard” bucket and it is quite difficult to see meaningful upside in the near-term on a risk-adjusted basis.”

So, what happened since then? Here’s a chart off Google Finance (a free resource that you can use), with my purple arrow showing the date on which the Sasol piece was published:

Did I think that things would get this bad for Sasol? No, I genuinely didn’t. Did I believe that the upside potential vs. downside risk made it worth having exposure? No, I certainly didn’t believe that and hence I didn’t hold shares.

The markets aren’t about being able to predict specific share prices. You’re fooling only yourself if you think you can get that right on a regular basis. Instead, it’s about assessing the opportunities vs. the risks and figuring out whether a specific position is worth it.

Sasol wasn’t worth it and I’m glad I avoided this nightmare.

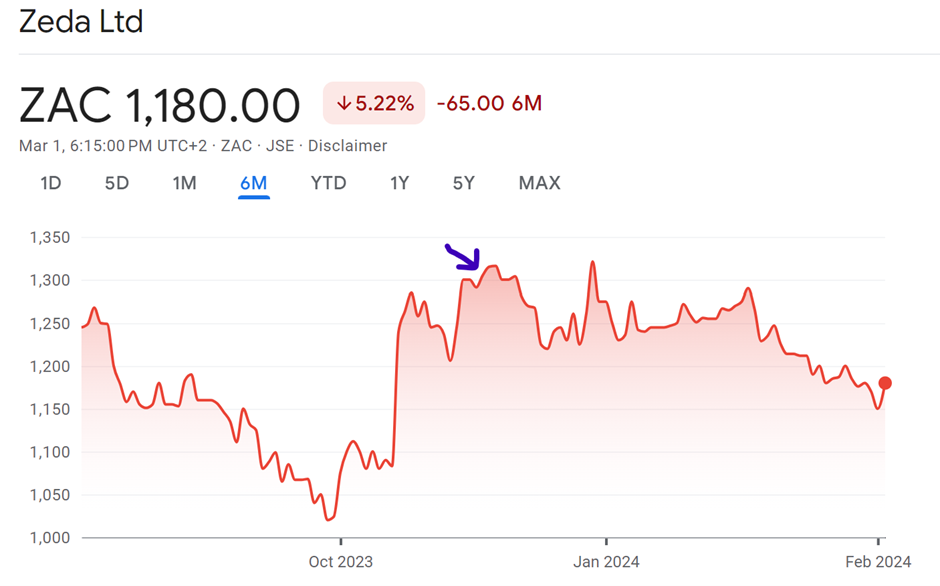

Zeda: published 4 December 2023

I’m a fan. That’s the long and the short of it. I think that Zeda offers some pretty compelling stuff to investors and is a good example of a South African business that trades at an appealing multiple.

There’s growth and there are strong existing returns on capital, so that ticks two of the most important boxes for any equity investment. There’s also a lot less debt than there used to be, which is another tick in the box.

Perhaps most importantly, Zeda should start paying dividends this year. Assuming that happens, I think that more investors will be willing to take a risk here and potentially push the price to a higher multiple.

Investing is about strategies and tactics. From a strategy perspective, I clearly like Zeda. From a tactical perspective, I didn’t like the sudden rally in the share price. These gaps usually close over time as investors take profit and the company slowly fades from the headlines.

Having said that, I also recognise the risk of waiting forever to get involved and then missing out. A great example is Spur, which leaped suddenly and didn’t just hold onto those gains, but managed to compound them.

Here’s exactly what I wrote:

“I’m tempted to wait for a pull-back after the recent rally. I’m also conscious that at this valuation multiple, I might be waiting forever for that pull-back.”

Thankfully, my patience in Zeda seems to be paying off, as the share price has dropped considerably since the publishing date (indicated with the arrow on this chart):

My trigger finger is getting very itchy on Zeda.

Looking ahead to the rest of March

This month, I’m turning my gaze offshore. The idea will be to expose you to some international stocks, with significant time spent on the underlying drivers of performance along with everything else.

Of course, that doesn’t mean that local stocks will be ignored. You can get my views on SENS every single day in Ghost Mail, for free!

Want to know more about the latest news?

Any opinions, news, research, reports, analyses, prices, or other information contained within this research is provided by an external contributor as general market commentary and does not constitute investment advice for the purposes of the Financial Advisory and Intermediary Services Act, 2002. First World Trader (Pty) Ltd t/a EasyEquities (“EasyEquities”) does not warrant the correctness, accuracy, timeliness, reliability or completeness of any information (i) contained within this research and (ii) received from third party data providers. You must rely solely upon your own judgment in all aspects of your investment and/or trading decisions and all investments and/or trades are made at your own risk. EasyEquities (including any of their employees) will not accept any liability for any direct or indirect loss or damage, including without limitation, any loss of profit, which may arise directly or indirectly from use of or reliance on the market commentary. The content contained within is subject to change at any time without notice.

Search all articles

Posts by topic

- Market News & Events

- Easy Community

- Education

- Dividends Update

- Exchange Traded Funds (ETFs)

- Property Investing

- Managed Bundles

- USD Wallet

- Retirement Annuity (RA)

- Cryptocurrency

- Tax Free Savings Account (TFSA)

- International Investing

- Unit Trusts

- New to Investing

- Artificial Intelligence

- EasyProtect

- EasyCredit

- Shares

- Government Bonds

- New Listings