Taking a look at what happened in the markets in September 2023.

Global Markets

The “September Effect” was in full force again this year as the broad-based selloff continued. The majority of asset classes closed the month in negative territory. The S&P 500 and MSCI World ended the month down 4.9% and 4.3% in USD respectively.

Interest rates were a key factor weighing on market sentiment in September. Most developed market central banks decided to keep interest rates unchanged in September, however they continued to caution of upside risks to inflation and reiterated their commitment to bring inflation down by continuing to hike rates. Consequently bond yields continued to rise, particularly US Treasuries.

Chart Source: BCA Research

Oil prices continued to rise in September due to an agreement between Saudi Arabia and Russia to prolong their production cut measures until the end of 2023. Furthermore, it is important to note that higher oil prices influences inflation to remain elevated.

The Dollar index continued its strong run in September against most currencies due to increased global uncertainty, sticky inflation and rising US yields.

Chart Source: Tradingview, DXY Performance

Emerging markets outperformed their Developed market counterparts, with the MSCI EM down 2.6% in USD with China remaining the biggest drag on Emerging Markets.

China’s Economic data continues to point towards a meaningful slowdown, and the follow through on Politburo’s stimulus announcement in July has been underwhelming – as we expected. Historically, Chinese stimulus programs have had a massive impact on global growth, particularly commodity-exporting emerging markets. However, high levels of debt, and a property bubble have taken away China’s ability to stimulate growth in recent years.

Chart: Chinese growth remains on downward trend (source: BCA Research)

Local Markets

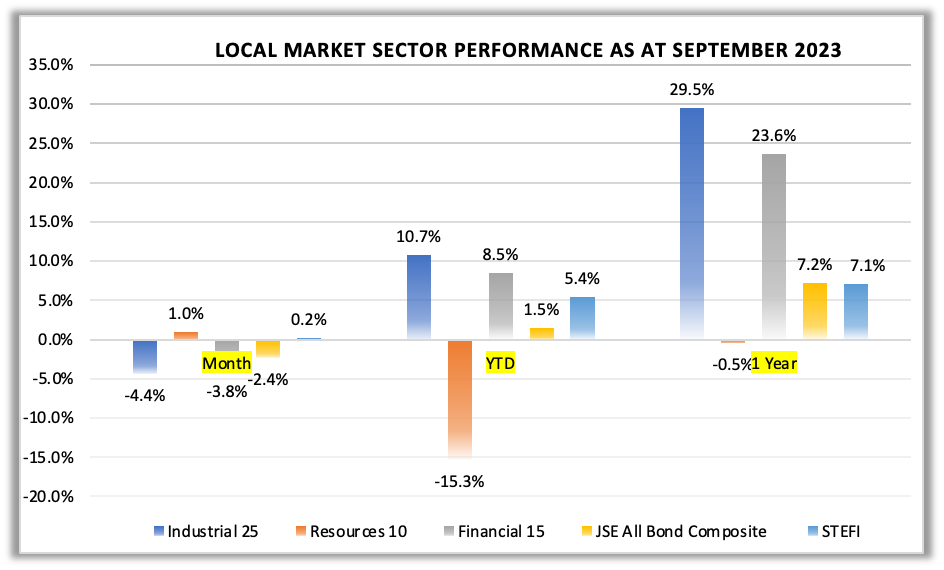

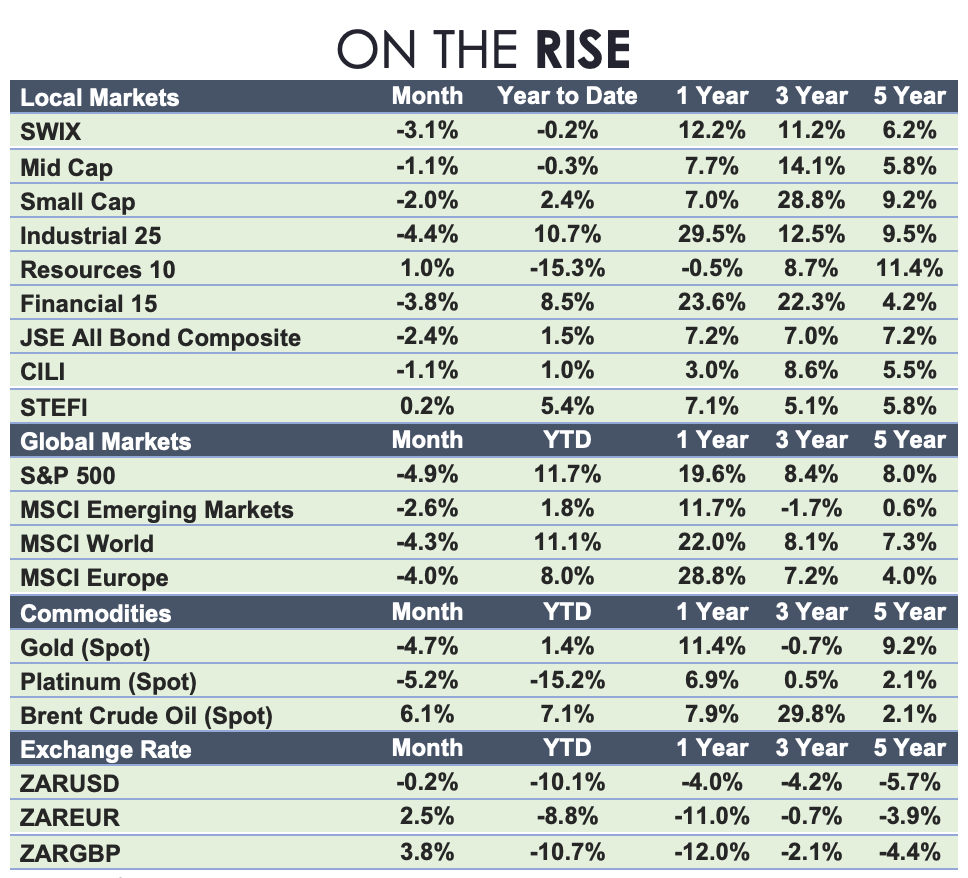

Local markets took their direction from global markets, with the JSE All Share Index falling 3.1% in ZAR. Losses on the JSE were fairly broad-based with the Financial 15 and Industrial 25 index ending the month down 3.8% and 4.4% respectively. Resources managed to deliver a small positive contribution for September as industrial metals held up.

Local government bonds sold off on concerns that global central banks may need to keep interest rates higher for longer. The JSE All Bond Composite and CILI lost 2.4% and 1.1% respectively.

Source: Infront

The high interest rates in South Africa are doing their job of bringing down inflation, which gave the SARB the leeway to pause interest rate hikes in September, a much needed break for the South African consumer. The repo rate now sits at 8.25%, making cash and money market instruments an attractive proposition to South African savers.

Chart Source: Infront

In September, the Rand held up relatively well against a generally strong US Dollar as rising global rates and global uncertainty saw investors continue to flock to the safety of the US Dollar. Despite multiple intra month spikes, the Rand closed slightly weaker at 18.91.

Source: Infront

Comments from our Chief Investment Officer, Duane Gilbert

Despite the “September Effect”, global markets remain resilient. Markets are confident that a recession will be avoided. We feel this is unlikely given the aggressiveness of interest rate hikes, at a time where global growth is fragile. Even if a recession can be avoided, valuations are too sanguine given the rapid withdrawal of liquidity, low global growth and high geopolitical risks. Fundamentally, the market environment remains unsupportive. As a result, we maintain a conservative positioning in our portfolios. Our exposure to global equities is low. Within equities we have taken a more defensive stance, favouring US quality equities and defensive sectors. We have a high allocation to global bonds which provide a strong hedge during a recession. South African equities are particularly cheap but vulnerable to a global sell-off. One needs to carefully pick companies that can grow their earnings in a low growth environment.

Our portfolios have a high allocation to SA Bonds (where longer-dated instruments are still offering double-digit yields) and exposure to commodity backed loans. We also hold a lot of cash in our portfolios. We prefer USD over ZAR. The sharp weakness we saw in August on the back of rather mild news is testament to how fragile the ZAR is. Our large cash position gives us the dry powder we need to take advantage of bargains that may arise from a market sell-off. Finally, we have a position in renewable energy infrastructure projects, which are not only attractive from an IRR perspective but will meaningfully increase electricity production and reduce carbon emissions in South Africa.

-2.png?width=1200&length=1200&name=image%20(10)-2.png)

Any opinions, news, research, reports, analyses, prices, or other information contained within this research is provided by an employee of EasyEquities an authorised FSP (FSP no 22588) as general market commentary and does not constitute investment advice for the purposes of the Financial Advisory and Intermediary Services Act, 2002. First World Trader (Pty) Ltd t/a EasyEquities (“EasyEquities”) does not warrant the correctness, accuracy, timeliness, reliability or completeness of any information (i) contained within this research and (ii) received from third party data providers. You must rely solely upon your own judgment in all aspects of your investment and/or trading decisions and all investments and/or trades are made at your own risk. EasyEquities (including any of their employees) will not accept any liability for any direct or indirect loss or damage, including without limitation, any loss of profit, which may arise directly or indirectly from use of or reliance on the market commentary. The content contained within is subject to change at any time without notice.

Search all articles

Posts by topic

- Market News & Events

- Easy Community

- Education

- Dividends Update

- Exchange Traded Funds (ETFs)

- Property Investing

- Managed Bundles

- USD Wallet

- Retirement Annuity (RA)

- Cryptocurrency

- Tax Free Savings Account (TFSA)

- International Investing

- Unit Trusts

- New to Investing

- Artificial Intelligence

- EasyProtect

- EasyCredit

- Shares

- Government Bonds

- New Listings