The Finance Ghost talks about why it might be good to have exposure to the US banking industry in your global portfolio. As exciting as the technology sector is, there’s a big and important world beyond the Magnificent Seven.

The Huskies of Wall Street: Why I own US banks

In my approach to building my portfolio, I believe that diversification across sectors is important. Hindsight is always very easy when looking back and wishing you had invested more in the best-performing sector on the market. If it was that easy to see this stuff in advance, then the markets would be terribly boring and everyone would be wealthy. That clearly isn’t the case.

For this reason, I make sure that I have exposure to the US banking industry in my global portfolio. As exciting as the technology sector is, there’s a big and important world beyond the Magnificent Seven.

It’s not exactly as though US banks are boring, either.

The home of capitalism

If you’re going to invest in the most capitalist activity in the world, it may as well be in the home of capitalism.

The banking industry in the US is exciting. The most famous names on Wall Street are all available to you in your EasyEquities USD account, letting you pick and choose from the world’s leading merchant banking groups and more traditional lenders.

At heart, banking is about taking risk. The Wolves of Wall Street are taking those risks every day through activities like leading IPOs and driving multi-billion-dollar mergers, backed up by highly structured debt financing packages. They raise bonds for clients and assist with global balance sheet structuring for the largest corporates on earth.

Stock option structures for key executives? You got it. And while they are at it, the executives can also entrust these banks with managing their entire personal portfolios. Right this way, sir and madam. We’ve been expecting you.

These days, those wolves have been tamed by compliance regulations that were highly necessary, as evidenced by the Global Financial Crisis. Less wolf, more husky. That’s a good thing.

We have a significantly more watered-down version of this in South Africa, with our banking groups primarily focused on more conservative banking activities. They have large full-service retail banking operations aimed at consumers across the income spectrum, which is an entirely different business model to the likes of Goldman Sachs.

Our conservative banking industry served us well during the Global Financial Crisis. In a low growth economy though, they struggle to generate exciting returns for investors. Instead of earning juicy fees on exciting listings, they are trying to balance the impairments on the home loans book. It’s just not the same out here.

The even bigger concern is that in order to generate solid returns on the global stage, they need to first overcome the hurdle of a structurally depreciating rand that never seems to want to find any strength.

Dollar dollar bill, y’all

The world is a big place. You are able to invest overseas as well as locally, which makes it a sensible approach to measure your wealth creation in global terms.

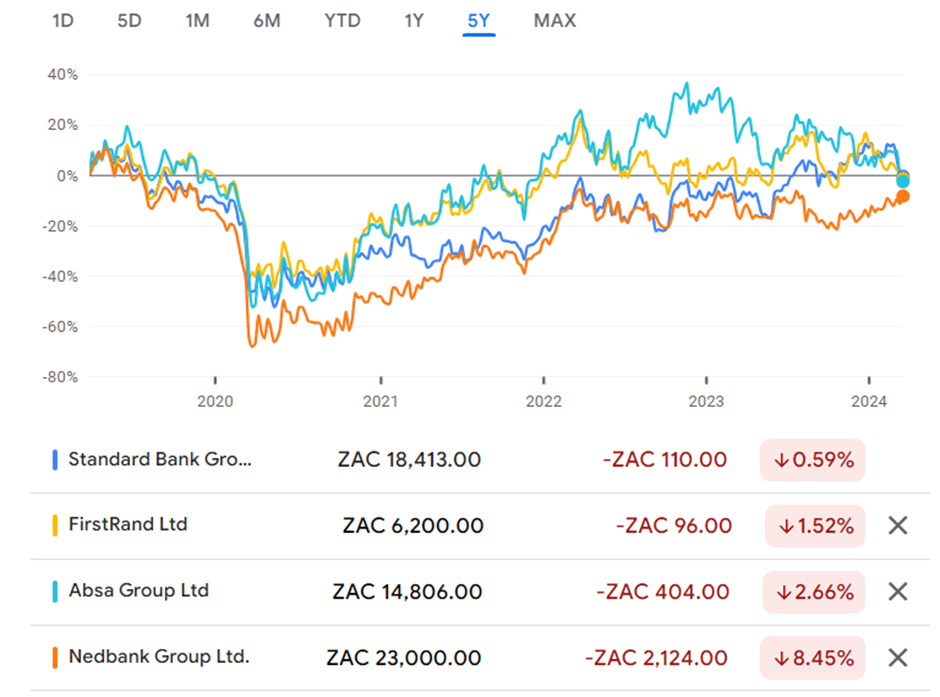

To kick off, here are the four largest South African banking groups with full-service retail banking offerings, charted over five years:

It’s not great, is it? This doesn’t show dividends of course, which would take these returns into the green. Still, it hasn’t been a happy time for the local banks over five years.

The two stars of the industry over the past five years deserve their own chart, showing what happens when you keep winning market share and evolving off a basic product range (Capitec) and the value of building a more exciting banking group with UK exposure as well (Investec):

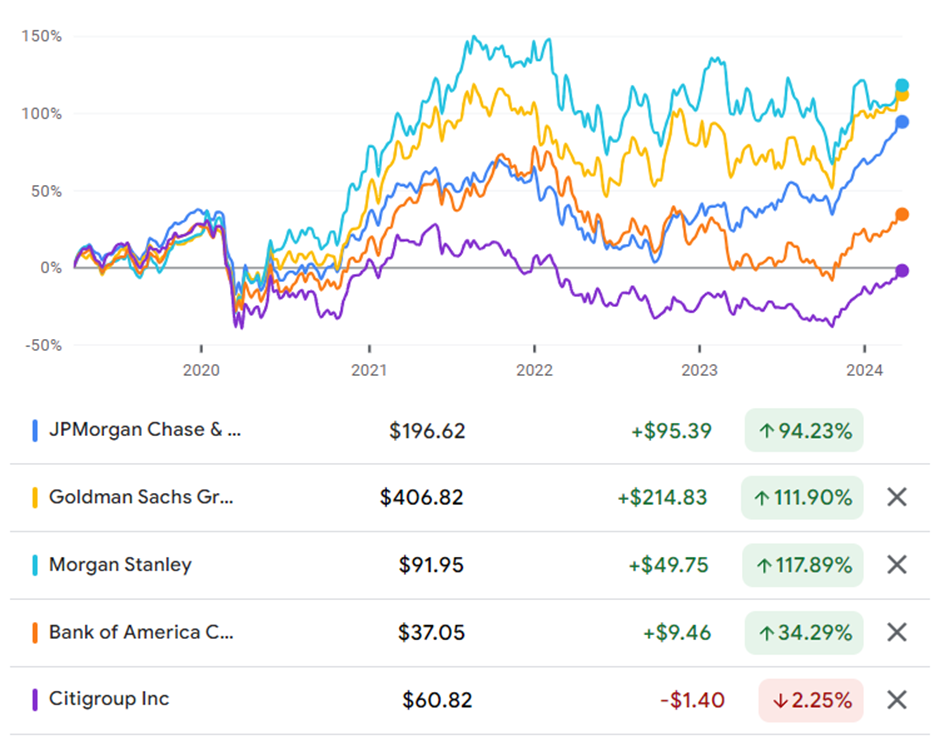

Before you pat yourself on the back too much about those local prospects and how they performed over five years, here are some of the US giants over the same period:

I thought it was only fair to include Citigroup as an example of how not to do it. After all, I don’t want to be accused of bias towards offshore wealth creation opportunities!

The critical thing to remember in the chart of US banks is that these are dollar share prices, which means dollar returns. If we are going to measure our wealth in global terms, we need to compare these returns to Capitec and Investec expressed in dollars rather than rands.

Over 5 years, the rand has been smashed from around R14.50 to the dollar to R19.00. Investec’s return of 138% reduces to around 82% in dollars, which means it underperformed three of the US banks on that chart. Capitec’s return is around 17.5% in dollars, which is even worse than Bank of America’s return and way off the leaders of the pack.

With Investec as the only local banking option that kept pace with the US alternatives over the past five years, perhaps it’s worth considering why the zebra bank has stood out from the rest of the local industry.

Right products in the right places

Full-service retail banking is a difficult way to make money. Branch networks are expensive and archaic, with digital banks continuously trying to disrupt this space. Also, broad credit exposure to South African consumers is generally not a good idea.

Where corporate and investment banking operations do perform well (thanks to trends like renewable energy and others), credit losses in the retail banking business tend to erode that benefit. On top of all this, South Africa offers very little economic growth to make things easier.

Investec’s strength has been a combination of its more focused approach (private banking rather than broad retail banking) and its exposure to the UK market, baking a rand hedge into the group. Even Standard Bank’s recent success vs. the other major peers is being driven by the performance in Africa rather than South Africa.

It seems as though the ingredients for success have been a combination of growth outside of South Africa and a focus on higher margin products that drive enhanced return on equity – the key valuation metric for banks.

Capitec is the exception here, with growth having come from incredible market share gains in the South African market. At some point though, that is likely to slow down. It says something that Capitec recently increased its stake in offshore-based Avafin Holdings.

Banking stalwarts

I like to invest my money where the ducks are quacking. The banking ducks are not quacking in South Africa. Yes, it’s absolutely possible to make money from shorter-term strategies around local banks, like valuation dislocations and relative plays. No, I’m not convinced that local retail banking groups will beat the returns available from US banks over the next decade.

The likes of JPMorgan Chase and Goldman Sachs are stalwarts in my portfolio. The latter is a more cyclical choice, as Goldman Sachs is strongly exposed to IPO activity and broader equity valuations. JPMorgan is a more diversified choice without venturing into the more traditional banking services that I don’t believe are attractive enough in the modern world.

My offshore portfolio helps me sleep easily at night, even when it includes a couple of wolves. Or huskies, for that matter.

Want to know more about the latest news?

Any opinions, news, research, reports, analyses, prices, or other information contained within this research is provided by an external contributor as general market commentary and does not constitute investment advice for the purposes of the Financial Advisory and Intermediary Services Act, 2002. First World Trader (Pty) Ltd t/a EasyEquities (“EasyEquities”) does not warrant the correctness, accuracy, timeliness, reliability or completeness of any information (i) contained within this research and (ii) received from third party data providers. You must rely solely upon your own judgment in all aspects of your investment and/or trading decisions and all investments and/or trades are made at your own risk. EasyEquities (including any of their employees) will not accept any liability for any direct or indirect loss or damage, including without limitation, any loss of profit, which may arise directly or indirectly from use of or reliance on the market commentary. The content contained within is subject to change at any time without notice.

Search all articles

Posts by topic

- Market News & Events

- Easy Community

- Education

- Dividends Update

- Exchange Traded Funds (ETFs)

- Property Investing

- Managed Bundles

- USD Wallet

- Retirement Annuity (RA)

- Cryptocurrency

- Tax Free Savings Account (TFSA)

- International Investing

- Unit Trusts

- New to Investing

- Artificial Intelligence

- EasyProtect

- EasyCredit

- Shares

- Government Bonds

- New Listings